Inflation, Interest Rates and Stock Market - Key Elements to Consider

Inflation, Interest Rates and Stock Market - Key Elements to Consider

May CPI Report Exceeds Expectations, a deep dive into the bullish catalyst for the week.

The relationship between inflation, interest rates, and the stock market is complex, but here's a breakdown of how they can affect each other:

High Inflation and Rising Interest Rates

High Inflation: When inflation is high, companies' costs rise, potentially leading to lower profits. Investors might become less enthusiastic about the stock market as a result.

Rising Interest Rates: The Federal Reserve raises interest rates to combat inflation. Higher interest rates make borrowing more expensive, which can slow down economic growth and potentially hurt corporate earnings. Additionally, higher rates make bonds a more attractive investment compared to stocks, potentially drawing money away from the stock market.

Disinflation and Interest Rate Decreases:

Disinflation: Disinflation, which is a slowdown in inflation, can be positive for the stock market. It suggests that price increases are coming under control, which can improve corporate profit margins.

Interest Rate Decreases: The Federal Reserve might lower interest rates to stimulate the economy during periods of disinflation or recession. Lower interest rates can make stocks more attractive compared to bonds, potentially leading to increased investment in the stock market.

Stock Market Impact:

Interest Rate Cuts Don't Always Mean Stock Market Gains: While falling interest rates can be a positive sign for stocks, it's not a guaranteed path to a rising market. The stock market often reacts to the reason behind the rate cuts.

If rate cuts are due to a strong economy and potential for future growth, the stock market might react positively.

However, if rate cuts are in response to a weakening economy or recession, the stock market might react negatively as it reflects a slowdown in corporate earnings.

Here are some additional factors to consider:

Company Earnings: Ultimately, stock prices are driven by a company's future earnings potential. Even during periods of disinflation and rate cuts, companies with strong earnings and growth prospects are likely to see their stock prices perform well.

Investor Sentiment: The overall sentiment of investors can also play a role. If investors are generally optimistic about the future, the stock market may react more favorably to disinflation and rate cuts.

Be Careful With What You Wish

Disinflation and interest rate decreases can be positive signs for the stock market, but the impact is not always straightforward. It depends on the reasons behind the disinflation and rate cuts, as well as overall economic conditions and investor sentiment.

Historically, the S&P 500 has experienced an average decline of 23.5% over a period of roughly 195 days following the initial Fed rate cut in a tightening cycle. It's important to consider this historical performance when anticipating the potential impact of future rate cuts.

The stock market is a forward-looking mechanism

This means investors don't just base their decisions on a company's current performance (sales, profits), Instead, they focus on the company's future potential.

Investors try to discount (estimate the present value of) a company's future earnings stream. This future stream of earnings could come from factors like:

Continued growth in sales

Expanding into new markets

Developing innovative products

Increasing profit margins

That said, at a corporate level things still look good considering the chart below.

CPI Context

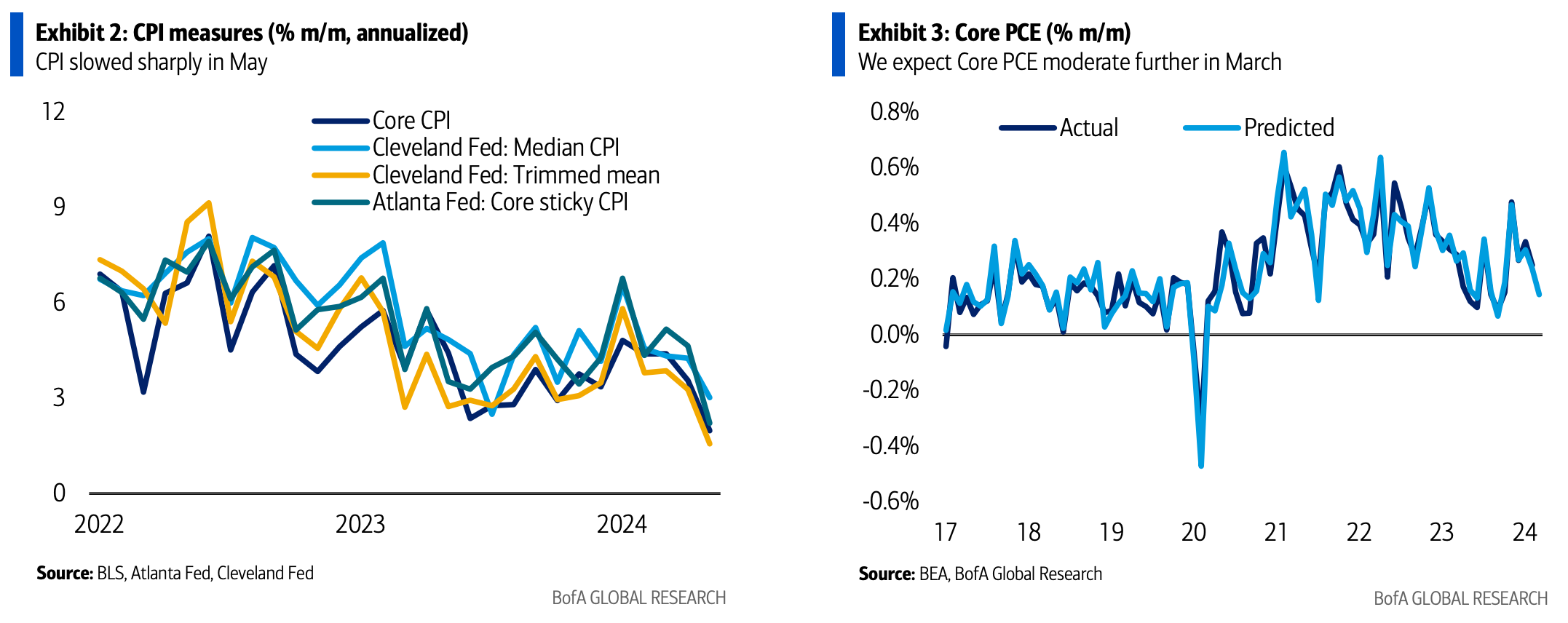

The continued improvement of CPI boosted the market this week, technically the charts suggested struggle at resistance levels, but a better than expected MAY CPI report injected a rally considering.

May's inflation data was a significant improvement over previous months, earning an "A" grade compared to Governor Waller's "C" for April.

Core inflation rose much less than expected (2% annualized), driven by a slowdown in core services and continued decline in core goods prices.

Alternative inflation measures also confirmed the moderation.

Bank Of America expects May core PCE inflation to be even lower (0.14-0.16% m/m), with headline PCE likely flat.

This positive data aligns with the Fed's goals, but more confirmation is needed before they consider easing rates.

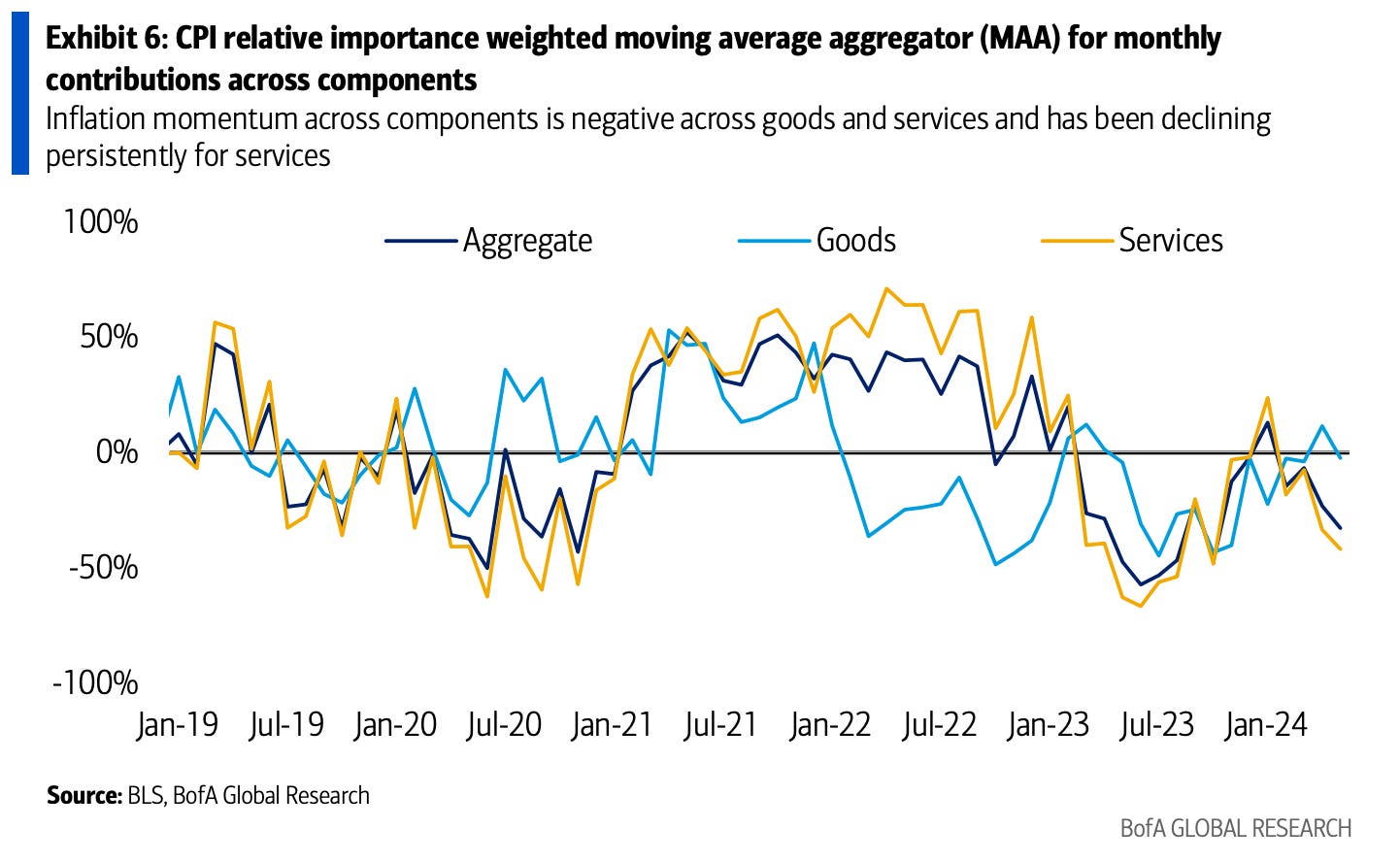

Inflation momentum is losing steam.

Earlier concerns about inflation picking back up haven't materialized.

This slowdown is particularly evident in services, a major contributor to overall inflation. Even though inflation for things like goods picked up slightly in the past year, the overall trend is still disinflationary (prices rising at a slower pace).

The recent shift in how different categories contribute to inflation, combined with the slowing momentum, suggests disinflation is likely to continue in the coming months, with services playing an even bigger role.

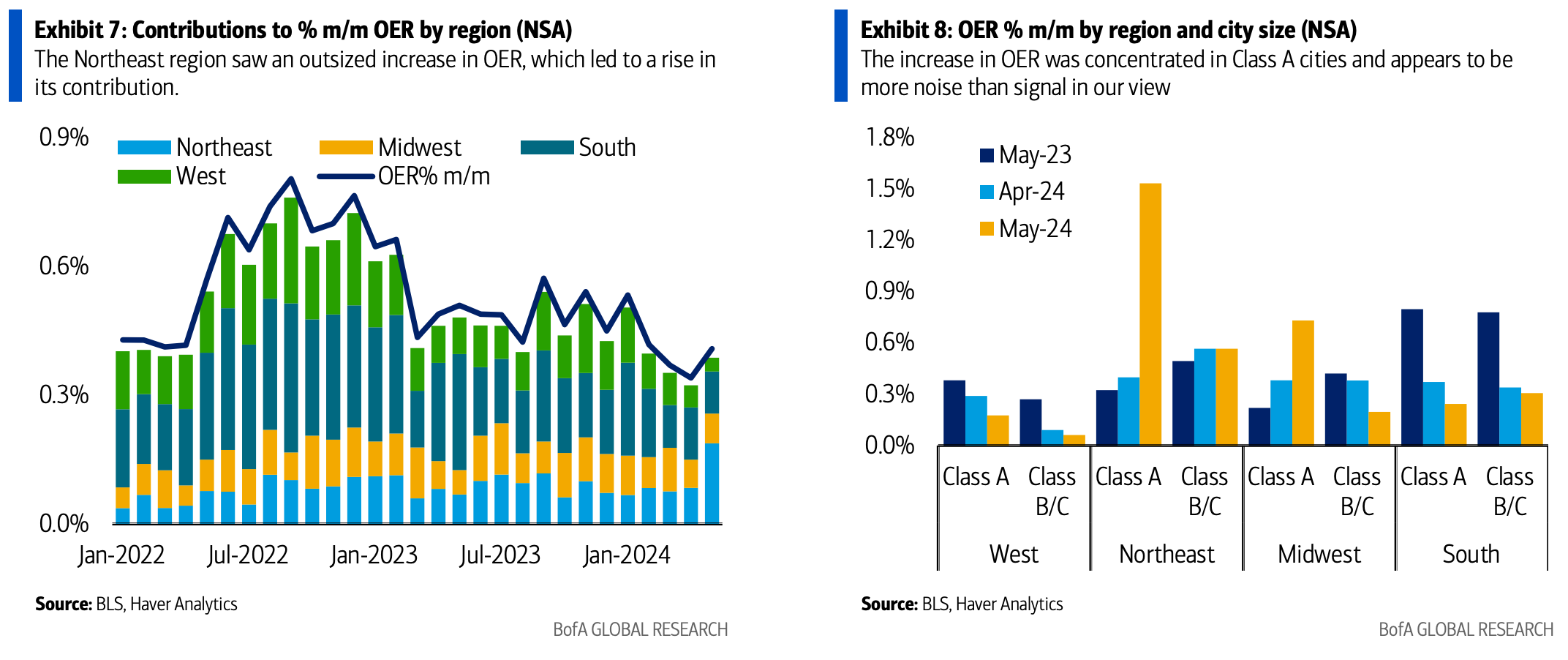

Northeast Rent Spike Likely Temporary

May's inflation report showed rent and OER (owner's equivalent rent) remaining elevated.

While the Northeast saw a significant increase in OER (particularly in major cities like New York and Philadelphia), Bank Of America’s expectation is more of an outlier than a long-term trend.

Expectation for OER inflation is to moderate in the coming months, particularly as the Northeast data normalizes.

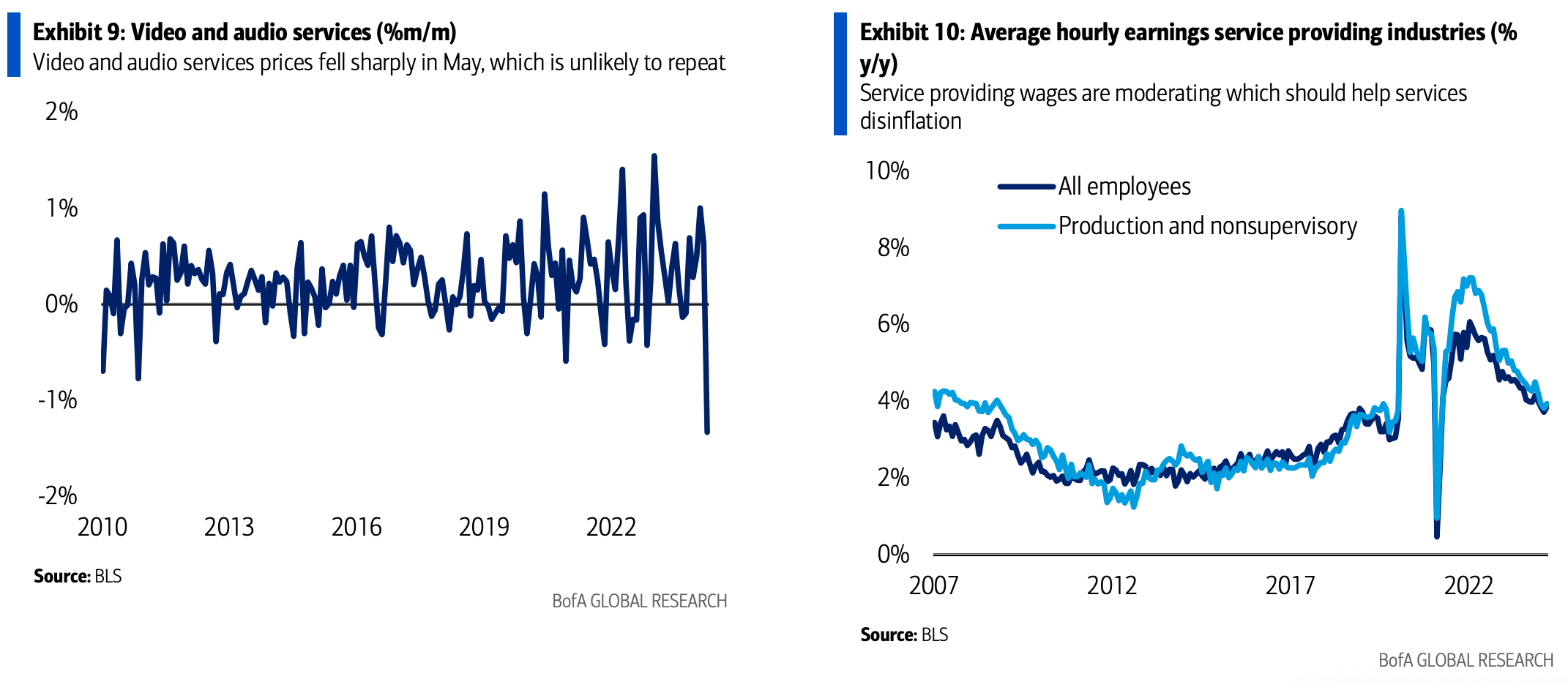

Non-Housing Services Inflation: Fading Short-Term Dips, Long-Term Disinflation Likely

The report showed some unexpected softness in non-housing services (excluding rent and OER). However, the authors believe this won't persist due to:

One-off factors: Declines in airfares and video/audio services likely won't repeat.

Normalization: Motor vehicle insurance price increases should moderate, not necessarily fall further.

Despite these temporary dips, the authors expect disinflation (slower price increases) to continue in non-housing services for two reasons:

Modest wage growth: The labor market is showing signs of balance, leading to slower wage increases which can translate to slower service price increases.

Moderation in motor vehicle insurance: Although not falling further, insurance price increases are likely to slow down.

CONCLUSIONS

Positive corporate outlooks and forecasts of rising earnings. Continuing bullish views for later this year are fueling optimism and driving up stock prices.

May CPI Points Toward Continued Disinflation. The latest inflation data suggests disinflationary pressures are broadening, with momentum tilting further negative. While this is a single report, it strengthens the case for inflation likely continuing to moderate over the medium term.

Disinflation could prompt the Fed to lower interest rates. However, historically, such rate cuts have been associated with stock market declines.

This is a secular bull market until it isn’t, rate cuts are definitely something to watch carefully, potentially by the end of the year.

This content is not intended to be investment advice.